When facing financial difficulties, individuals often find themselves at a crossroads, weighing the merits of debt relief against debt consolidation. Both strategies aim to alleviate the burden of overwhelming debt, but they operate in fundamentally different ways. This comprehensive analysis delves into the advantages and disadvantages of each approach, providing crucial insights for those navigating the complex landscape of personal finance.

| Pros | Cons |

|---|---|

| Potential for significant debt reduction | Negative impact on credit score |

| Simplified payment structure | Risk of accumulating more debt |

| Possibility of lower interest rates | Potential tax implications |

| Faster debt repayment timeline | Fees associated with services |

| Relief from creditor harassment | Not all debts may be eligible |

Debt Relief: A Closer Look

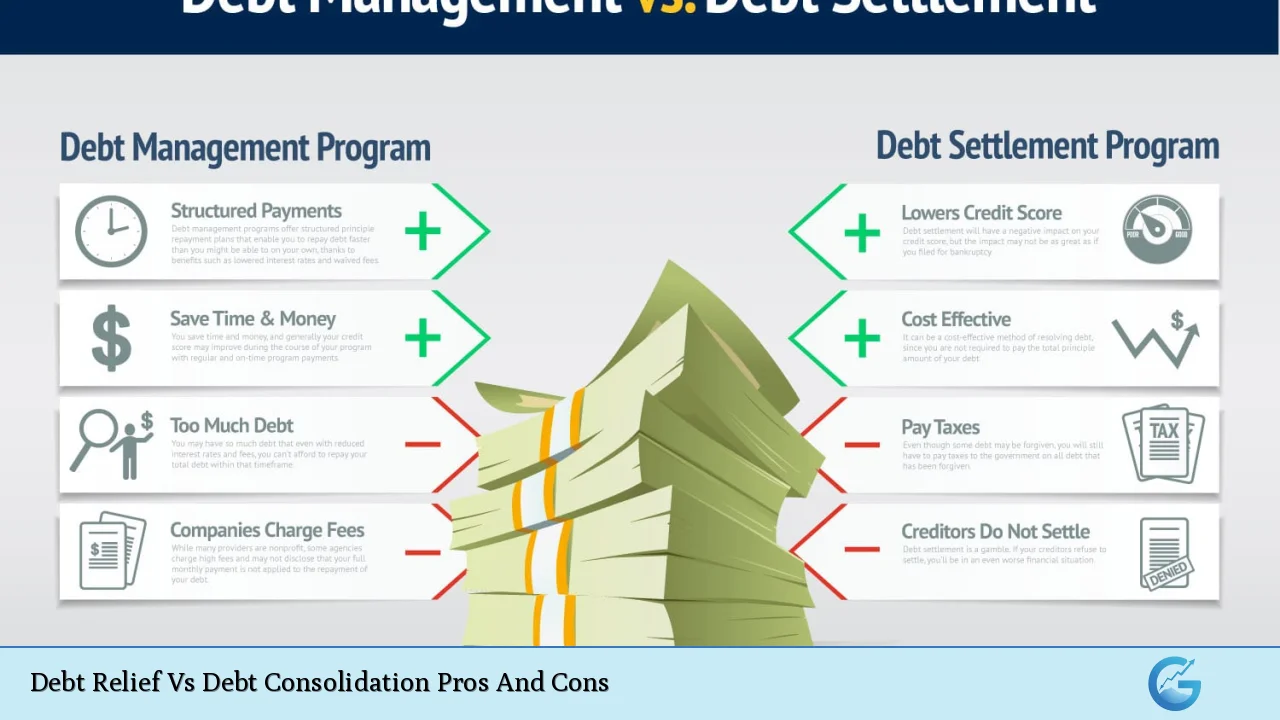

Debt relief, often referred to as debt settlement, is a strategy that involves negotiating with creditors to reduce the total amount owed. This approach can be particularly appealing for individuals struggling with substantial unsecured debts, such as credit card balances or personal loans.

Advantages of Debt Relief

- Significant Debt Reduction: The primary allure of debt relief is the potential for substantial debt reduction. In some cases, creditors may agree to forgive up to 50% or more of the outstanding balance.

- Faster Path to Debt Freedom: By reducing the total amount owed, debt relief can offer a quicker route to becoming debt-free compared to making minimum payments over an extended period.

- Single Monthly Payment: Many debt relief programs consolidate multiple debts into a single monthly payment, simplifying the repayment process for the debtor.

- Potential End to Creditor Harassment: Once enrolled in a debt relief program, many individuals experience a reduction in creditor calls and collection efforts.

Disadvantages of Debt Relief

- Credit Score Impact: Debt relief can significantly damage your credit score, as settled accounts are typically reported as “settled for less than the full balance” on credit reports. This negative mark can persist for up to seven years.

- Tax Implications: The IRS may consider forgiven debt as taxable income. This means that individuals who have successfully settled their debts may face an unexpected tax bill.

- Fees: Debt relief companies often charge substantial fees for their services, typically a percentage of the debt enrolled or the amount saved.

- No Guarantee of Success: There’s no assurance that creditors will agree to settle debts. Some may refuse to negotiate, potentially leaving the debtor in a worse financial position.

- Potential for Legal Action: During the debt settlement process, creditors may choose to pursue legal action to recover the full amount owed.

Debt Consolidation: Streamlining Your Finances

Debt consolidation involves combining multiple debts into a single loan or credit line, often with the aim of securing a lower interest rate or more favorable repayment terms.

Advantages of Debt Consolidation

- Simplified Repayment: By consolidating multiple debts into one, borrowers can streamline their finances and reduce the risk of missed payments.

- Potential for Lower Interest Rates: Depending on the individual’s credit score and market conditions, debt consolidation may offer access to lower interest rates, potentially saving money over time.

- Fixed Repayment Schedule: Many debt consolidation loans come with fixed interest rates and repayment terms, providing predictability and stability in budgeting.

- Possible Credit Score Improvement: If managed responsibly, debt consolidation can lead to improved credit scores over time as debts are paid down and payment history remains positive.

- Preservation of Credit Accounts: Unlike debt settlement, consolidation typically doesn’t require closing credit accounts, which can be beneficial for maintaining credit history length.

Disadvantages of Debt Consolidation

- Collateral Risk: Some consolidation loans, particularly home equity loans or lines of credit, may require collateral, putting valuable assets at risk if payments are not maintained.

- Potential for Higher Total Interest: While monthly payments may be lower, extending the repayment term could result in paying more interest over the life of the loan.

- Temptation to Accumulate More Debt: After consolidating, some individuals may be tempted to use their newly available credit lines, potentially worsening their debt situation.

- Fees and Costs: Consolidation loans may come with origination fees, balance transfer fees, or closing costs, which should be factored into the overall cost analysis.

- Qualification Challenges: Securing a consolidation loan with favorable terms typically requires a good credit score, which may be difficult for those already struggling with debt.

Making the Right Choice: Factors to Consider

When deciding between debt relief and debt consolidation, several factors should be carefully evaluated:

- Total Debt Amount: Debt relief may be more suitable for those with high unsecured debt balances, while consolidation can be effective for managing multiple smaller debts.

- Credit Score: Individuals with good credit scores may benefit more from consolidation, as they’re likely to qualify for better interest rates.

- Type of Debt: Debt relief typically works best for unsecured debts, while consolidation can encompass a broader range of debt types.

- Long-Term Financial Goals: Consider how each option aligns with your long-term financial objectives, including homeownership or future borrowing needs.

- Risk Tolerance: Assess your comfort level with the potential risks associated with each strategy, such as credit score impact or asset exposure.

The Role of Professional Guidance

Given the complexity and potential long-term implications of both debt relief and consolidation, seeking professional advice is often advisable. Certified financial planners, credit counselors, or reputable debt management companies can provide personalized guidance based on your specific financial situation.

It’s crucial to thoroughly research any debt relief or consolidation company before engaging their services, as the industry has been known to attract unscrupulous operators. Look for accreditations from organizations such as the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA).

Alternatives to Consider

While debt relief and consolidation are popular options, they’re not the only strategies available for managing debt. Other alternatives to explore include:

- Debt Management Plans (DMPs): Offered by credit counseling agencies, DMPs can help negotiate lower interest rates and fees with creditors while providing a structured repayment plan.

- Balance Transfer Credit Cards: For those with good credit, transferring high-interest debt to a card with a 0% introductory APR period can provide temporary relief and savings.

- Bankruptcy: While often considered a last resort, bankruptcy can offer a fresh start for those facing insurmountable debt. However, it comes with significant long-term consequences and should be carefully considered with legal counsel.

The Importance of Financial Education

Regardless of the debt management strategy chosen, developing strong financial literacy skills is crucial for long-term success. Many organizations offer free or low-cost financial education resources, covering topics such as budgeting, saving, and responsible credit use.

By addressing the root causes of debt accumulation and developing healthy financial habits, individuals can work towards not only resolving their current debt issues but also building a more stable financial future.

Conclusion

The choice between debt relief and debt consolidation is highly personal and depends on a variety of factors unique to each individual’s financial situation. While debt relief offers the potential for significant debt reduction, it comes with substantial risks to credit scores and potential tax implications. Debt consolidation, on the other hand, provides a path to simplify repayment and potentially save on interest, but may not address the underlying debt amount.

Ultimately, the most effective approach may involve a combination of strategies, coupled with a commitment to financial education and responsible money management. By carefully weighing the pros and cons of each option and seeking professional advice when needed, individuals can chart a course towards financial stability and freedom from the burden of overwhelming debt.

Frequently Asked Questions About Debt Relief Vs Debt Consolidation Pros And Cons

- How long does debt relief or consolidation typically take?

Debt relief programs often last 2-4 years, while debt consolidation loans typically have terms of 3-5 years. The duration can vary based on the amount of debt and the specific terms of the program or loan. - Can I include all types of debt in relief or consolidation programs?

Debt relief typically works best for unsecured debts like credit cards and personal loans. Debt consolidation can often include a wider range of debts, including secured loans, depending on the consolidation method chosen. - Will debt relief or consolidation stop collection calls?

Debt relief programs may reduce collection calls once creditors agree to the program. Debt consolidation can stop collection calls immediately for the debts included in the consolidation, as those debts are paid off with the new loan. - How much does debt relief or consolidation cost?

Debt relief companies typically charge 15-25% of the enrolled debt amount. Debt consolidation costs vary but may include origination fees, balance transfer fees, or closing costs, depending on the type of consolidation. - Can I get a debt consolidation loan with bad credit?

While it’s more challenging, some lenders offer debt consolidation loans for those with less-than-perfect credit. However, interest rates may be higher, potentially reducing the benefits of consolidation. - Is it possible to negotiate with creditors on my own instead of using a debt relief company?

Yes, it’s possible to negotiate directly with creditors. This approach can save on fees but requires time, persistence, and negotiation skills. Some creditors may be more willing to work with individuals directly. - How do debt relief and consolidation affect my ability to get credit in the future?

Debt relief can significantly impact credit scores and may make obtaining new credit difficult for several years. Debt consolidation, if managed responsibly, can have a more positive long-term effect on creditworthiness. - Are there any tax benefits to debt consolidation?

In some cases, the interest paid on a debt consolidation loan may be tax-deductible, particularly if it’s a home equity loan used to consolidate debt. However, it’s important to consult with a tax professional for specific advice.