Investing in annuities is a financial strategy that many individuals consider, especially those planning for retirement. Annuities are insurance products designed to provide a steady income stream, typically during retirement, in exchange for an initial investment. They can be appealing due to their promise of guaranteed income and tax-deferred growth. However, like any investment, they come with their own set of advantages and disadvantages. This article explores the pros and cons of investing in annuities, helping you make an informed decision about whether they align with your financial goals.

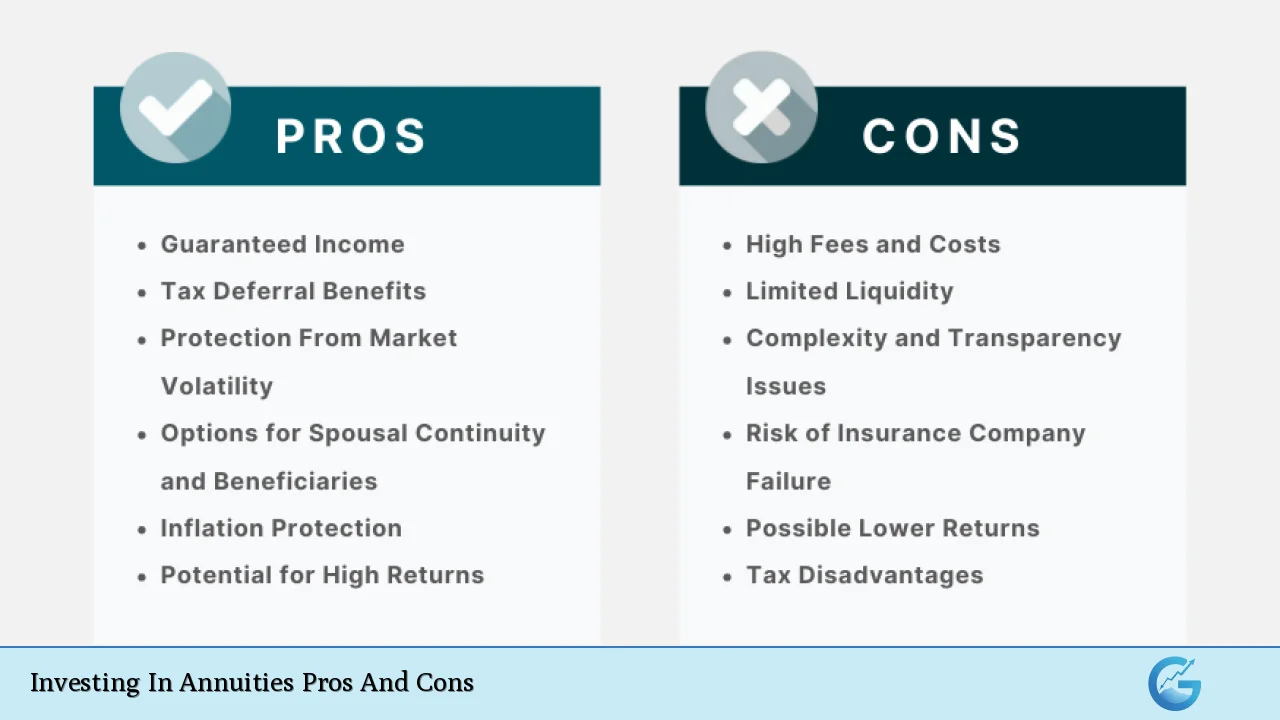

| Pros | Cons |

|---|---|

| Guaranteed income for life | High fees and commissions |

| Tax-deferred growth | Limited liquidity and access to funds |

| Protection against market volatility | Complexity and lack of transparency |

| Customizable options for different needs | Poor returns compared to other investments |

| Death benefits for beneficiaries | Risk of insurer default |

| Inflation protection with certain types | Difficult exit strategies and surrender charges |

| Long-term financial security | Potential tax implications on withdrawals |

| Structured payments can aid budgeting | Irreversible once purchased |

Guaranteed Income for Life

One of the most significant advantages of annuities is their ability to provide a guaranteed income for life. This feature is particularly appealing to retirees who are concerned about outliving their savings.

- Steady cash flow: Annuities can offer a reliable source of income that can help cover living expenses.

- Longevity risk mitigation: By ensuring a continuous income stream, annuities protect against the risk of depleting retirement savings.

- Peace of mind: Knowing that you have a guaranteed income can alleviate financial anxiety during retirement.

High Fees and Commissions

Despite their benefits, annuities often come with high fees and commissions, which can significantly impact your overall returns.

- Management fees: Many annuities charge annual fees that can erode your investment gains over time.

- Surrender charges: If you need to withdraw funds before the contract term ends, hefty surrender fees may apply.

- Commission-driven sales: Agents selling annuities often earn high commissions, which may incentivize them to recommend products that are not necessarily in the best interest of the investor.

Tax-Deferred Growth

Annuities allow for tax-deferred growth, meaning that you won’t pay taxes on your earnings until you withdraw them.

- Increased compounding: This tax advantage can lead to greater accumulation of wealth over time compared to taxable investments.

- Flexible contributions: Non-qualified annuities do not have annual contribution limits, allowing for potentially larger investments.

- Tax benefits upon withdrawal: Depending on your tax bracket at retirement, you may pay less in taxes when withdrawing funds than if you had been taxed annually.

Limited Liquidity and Access to Funds

A notable disadvantage of annuities is their limited liquidity, which can restrict access to your money when needed.

- Surrender periods: Many contracts include surrender periods during which withdrawals incur penalties.

- Access restrictions: Once you begin receiving payments, accessing additional funds from the account may not be possible without penalties.

- Emergency fund concerns: This lack of liquidity can pose challenges if unexpected expenses arise during retirement.

Protection Against Market Volatility

Annuities provide a level of protection against market volatility, particularly fixed and indexed varieties.

- Fixed returns: Fixed annuities guarantee a minimum interest rate, shielding investors from market downturns.

- Indexed options: Indexed annuities link returns to a stock market index while providing downside protection against losses.

- Stable income source: This characteristic makes them appealing to conservative investors looking for stability in uncertain markets.

Complexity and Lack of Transparency

Annuities can be complex financial products that often lack transparency regarding their fees and terms.

- Difficult to understand: The various types of annuities (fixed, variable, indexed) and their associated features can be confusing for investors.

- Hidden costs: Many investors may not fully grasp the extent of fees until they see reduced returns after several years.

- Need for professional guidance: Navigating these complexities often requires the assistance of a knowledgeable financial advisor.

Customizable Options for Different Needs

Annuities offer various customizable options that allow investors to tailor their contracts according to personal needs and preferences.

- Riders and add-ons: Features such as inflation protection or guaranteed minimum withdrawals can enhance the basic contract terms.

- Flexible payout structures: Investors can choose between lump-sum payments or structured payouts based on their financial situation.

- Beneficiary options: Some annuities allow for death benefits that ensure your beneficiaries receive funds upon your passing.

Poor Returns Compared to Other Investments

While annuities provide security, they often yield lower returns compared to other investment vehicles like stocks or mutual funds.

- Investment performance limitations: Variable annuities may underperform due to high fees associated with managing the underlying investments.

- Inflation risk: Fixed-rate annuities may not keep pace with inflation over time, resulting in decreased purchasing power.

- Opportunity cost: Money locked into an annuity could potentially earn higher returns if invested elsewhere in more aggressive assets.

Death Benefits for Beneficiaries

Many annuity contracts include provisions for death benefits, ensuring that beneficiaries receive a payout upon the owner’s death.

- Financial security for loved ones: This feature provides peace of mind knowing that your family will have financial support after your passing.

- Varied options available: Depending on the contract type, beneficiaries may receive either the remaining account balance or a predetermined amount.

Risk of Insurer Default

Investing in an annuity carries the risk associated with the issuing insurance company’s financial stability.

- Insurance company solvency: If an insurance company goes bankrupt, policyholders may lose their investment unless state guaranty associations cover it (up to certain limits).

- Importance of ratings: It’s crucial to choose an insurer with strong financial ratings from independent agencies to mitigate this risk.

Difficult Exit Strategies and Surrender Charges

Exiting an annuity contract can be challenging due to surrender charges and restrictions on withdrawals.

- High penalties for early withdrawal: Investors may face significant fees if they attempt to access their funds before the surrender period ends.

- Long-term commitment required: Annuities are designed as long-term investments; thus, withdrawing early often results in substantial losses.

Potential Tax Implications on Withdrawals

Withdrawals from an annuity can have tax implications that investors should consider carefully.

- Ordinary income tax rates apply: Earnings withdrawn are taxed as ordinary income rather than capital gains, which could lead to higher tax liabilities depending on your tax bracket at withdrawal time.

- Early withdrawal penalties: Withdrawals made before age 59½ may incur additional penalties, further reducing net gains from the investment.

Irreversible Once Purchased

Once you purchase an annuity, it is generally irreversible.

- No turning back: After committing funds into an annuity contract, you cannot change your mind without incurring penalties or losing benefits.

- Long-term planning required: Investors must carefully consider their long-term financial goals before making such a commitment as there is no flexibility post-purchase.

In conclusion, investing in annuities presents both significant advantages and notable disadvantages. They offer guaranteed income streams and tax-deferred growth but come with high fees, limited liquidity, and potential risks related to insurer defaults. Understanding these factors is crucial for anyone considering an annuity as part of their retirement strategy. As with any investment decision, consulting with a qualified financial advisor is recommended to ensure that an annuity aligns with your overall financial goals and risk tolerance.

Frequently Asked Questions About Investing In Annuities Pros And Cons

- What are the main benefits of investing in an annuity?

Annuities provide guaranteed lifetime income, tax-deferred growth on earnings, protection against market volatility, customizable options based on individual needs, and death benefits for beneficiaries. - What are some common drawbacks associated with annuities?

The main drawbacks include high fees and commissions, limited liquidity due to surrender charges, complexity in understanding terms and conditions, lower returns compared to other investments, and risks associated with insurer default. - How do taxes work with annuity withdrawals?

Withdrawals from an annuity are taxed as ordinary income rather than capital gains; early withdrawals before age 59½ may also incur additional penalties. - Can I lose money with an annuity?

You cannot lose money in the traditional sense; however, if the issuing insurance company defaults or if you withdraw early incurring penalties or high fees could lead to losses. - What types of annuities are available?

The main types include fixed annuities (guaranteed rates), variable annuities (investment-linked), indexed annuities (linked to market indices), and immediate or deferred payout options. - Are there any inflation-protected options within annuities?

Yes, some types of annuities offer inflation protection through escalating payouts that adjust according to inflation rates. - How do I choose a reliable insurance company for my annuity?

Select a company rated highly by independent agencies like A.M. Best or Standard & Poor’s; this indicates strong financial health and reliability. - Is it advisable to consult a financial advisor before investing in an annuity?

Yes, consulting a financial advisor is highly recommended as they can help assess whether an annuity aligns with your overall retirement strategy and financial goals.