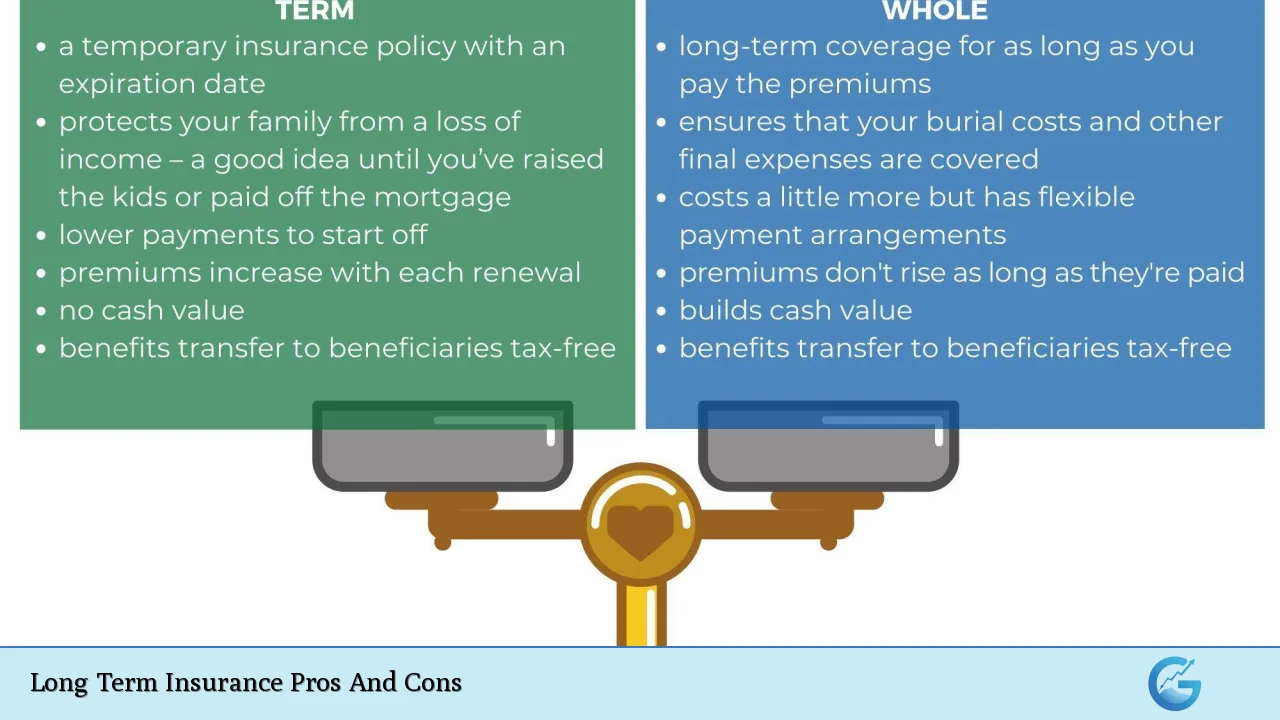

Long-term care insurance (LTCI) is designed to cover the costs associated with prolonged care needs that arise due to chronic illness, disability, or aging. As individuals live longer, the likelihood of requiring long-term care increases, making LTCI an important consideration for many. This insurance can help protect assets, provide peace of mind, and ensure that individuals receive the care they need without depleting their savings. However, it is essential to weigh the advantages against the disadvantages before making a decision. This article explores the pros and cons of long-term care insurance in detail.

| Pros | Cons |

|---|---|

| Protects savings from high long-term care costs | Premiums can be expensive and may increase over time |

| Offers tax-free benefits for long-term care claims | Policies may not cover all expenses or services needed |

| Provides flexibility in choosing care providers | Potential loss of premiums if care is never needed |

| Can be tailored to individual needs and budgets | Eligibility for coverage can be limited by health conditions |

| Offers inflation protection through benefit increases | Complex policies can be difficult to understand and compare |

| Gives peace of mind regarding future care needs | May require extensive medical underwriting for approval |

| Can help maintain independence in later years | Some policies have waiting periods before benefits kick in |

| Can preserve family assets for heirs | Not all policies are guaranteed renewable or stable in pricing |

Protects Savings from High Long-Term Care Costs

One of the most significant advantages of long-term care insurance is its ability to protect your savings. Long-term care can be prohibitively expensive, with costs for nursing homes or assisted living facilities often reaching hundreds of thousands of dollars per year.

- Financial Protection: LTCI helps shield your assets from being depleted by these high costs, ensuring that you do not exhaust your savings.

- Peace of Mind: Knowing that you have a financial safety net allows you to focus on your health and well-being rather than worrying about finances.

Offers Tax-Free Benefits for Long-Term Care Claims

Another advantage of long-term care insurance is that the benefits received are generally tax-free.

- Tax Benefits: In many cases, premiums paid may also be tax-deductible, providing additional financial relief.

- Financial Planning: This tax advantage makes LTCI an attractive option for those looking to manage their finances effectively as they age.

Provides Flexibility in Choosing Care Providers

Long-term care insurance typically offers policyholders the flexibility to choose their caregivers and settings.

- Choice of Care: You can select between home health aides, assisted living facilities, or nursing homes based on your preferences.

- Personalized Care: This flexibility allows you to receive care in an environment where you feel most comfortable.

Can Be Tailored to Individual Needs and Budgets

LTCI policies can be customized according to individual needs and financial situations.

- Customizable Coverage: You can decide on coverage amounts, benefit periods, and additional features like inflation protection.

- Budget-Friendly Options: This customization ensures that you can find a policy that fits within your financial means while still providing necessary coverage.

Offers Inflation Protection Through Benefit Increases

Many long-term care insurance policies include options for inflation protection.

- Increasing Coverage: This feature helps ensure that your benefits keep pace with rising healthcare costs over time.

- Future Security: By having inflation protection, you are less likely to face a shortfall in coverage as costs increase.

Gives Peace of Mind Regarding Future Care Needs

Having long-term care insurance provides significant peace of mind.

- Security for the Future: Knowing that you have a plan in place for potential future needs alleviates anxiety about aging and health issues.

- Support for Family Members: It also reduces the burden on family members who might otherwise have to provide care or support financially.

Can Help Maintain Independence in Later Years

Long-term care insurance can assist individuals in maintaining their independence as they age.

- In-home Care Options: Many policies cover home health services, allowing individuals to receive care while remaining in their own homes.

- Quality of Life: This option can significantly enhance quality of life by enabling seniors to live comfortably without relocating to a facility.

Can Preserve Family Assets for Heirs

Investing in long-term care insurance can help preserve family wealth.

- Asset Protection: By covering potential long-term care expenses through insurance, you can leave more assets intact for your heirs.

- Financial Legacy: This preservation helps ensure that your family has financial resources available after your passing.

Premiums Can Be Expensive and May Increase Over Time

Despite its benefits, one major drawback of long-term care insurance is the cost associated with premiums.

- High Initial Costs: Premiums can be substantial, especially for comprehensive coverage plans.

- Future Increases: Additionally, there is a risk that premiums will increase over time, potentially making it unaffordable later in life.

Policies May Not Cover All Expenses or Services Needed

Long-term care insurance does not always cover every type of service or expense related to long-term care.

- Limited Coverage: Many policies have specific exclusions or limitations on what services are covered.

- Out-of-Pocket Costs: This limitation may result in unexpected out-of-pocket expenses if additional services are required beyond what is covered by the policy.

Potential Loss of Premiums If Care Is Never Needed

Another significant disadvantage is the possibility of losing premiums paid if long-term care is never utilized.

- “Use It or Lose It” Model: Many traditional LTCI policies operate on this model, meaning if you do not require long-term care, you may not see any return on your investment.

- Financial Risk: This aspect can deter individuals from purchasing policies if they are uncertain about their future healthcare needs.

Eligibility for Coverage Can Be Limited by Health Conditions

Accessing long-term care insurance may be challenging due to health-related eligibility requirements.

- Medical Underwriting: Most insurers require medical underwriting before issuing a policy; pre-existing conditions may disqualify applicants.

- Age Considerations: The best time to purchase LTCI is often younger when health conditions are less likely to impact eligibility.

Complex Policies Can Be Difficult to Understand and Compare

The intricacies involved in different LTCI policies can lead to confusion among potential buyers.

- Variety of Options: With numerous types of policies available (stand-alone vs. hybrid), understanding each option’s benefits and drawbacks can be overwhelming.

- Need for Research: Prospective buyers must conduct thorough research and possibly consult with financial advisors to make informed decisions.

Some Policies Have Waiting Periods Before Benefits Kick In

Many long-term care insurance policies include elimination periods before benefits become available.

- Waiting Periods: This means there could be a delay between when you need assistance and when your policy starts paying benefits.

- Planning Ahead: Understanding these waiting periods is crucial for effective planning and ensuring adequate coverage when needed.

Not All Policies Are Guaranteed Renewable or Stable in Pricing

Finally, not all long-term care insurance policies guarantee renewal or stable pricing throughout their duration.

- Renewal Risks: Some insurers might change terms or deny renewal based on health status changes over time.

- Price Volatility: Consumers should carefully assess the stability of premium pricing before committing to a policy.

In conclusion, while long-term care insurance offers several advantages such as financial protection against high healthcare costs and peace of mind regarding future needs, it also comes with notable disadvantages including high premiums and potential limitations on coverage. Individuals must carefully evaluate their personal circumstances and consider both the pros and cons before investing in a policy.

Frequently Asked Questions About Long Term Insurance

- What is long-term care insurance?

A type of insurance designed to cover costs associated with prolonged healthcare needs due to chronic illnesses or disabilities. - How much does long-term care insurance typically cost?

The cost varies widely depending on age, health status, and coverage options but can range from $1,500 to $3,000 annually. - Is it worth getting long-term care insurance?

This depends on individual circumstances; it provides security but requires careful consideration due to potential costs. - At what age should I purchase long-term care insurance?

The ideal age is typically between 50 and 65 when premiums are lower and health conditions are less likely to affect eligibility. - What happens if I never use my long-term care insurance?

If you never use it, premiums paid may not be refunded; it’s often considered a “use it or lose it” product. - Can I customize my long-term care policy?

Yes, many policies allow customization regarding coverage amounts and additional features like inflation protection. - Are benefits from long-term care insurance taxable?

No, benefits received from qualified long-term care policies are generally tax-free. - If I move states, will my policy still be valid?

Most policies remain valid across state lines; however, it’s essential to check with your insurer regarding specific terms.