Refinancing a car loan is a financial decision that can significantly impact your monthly budget and overall financial health. This process involves replacing your existing auto loan with a new one, typically with different terms or a lower interest rate. For those navigating the complex world of personal finance, understanding the intricacies of auto loan refinancing is crucial. Whether you’re looking to reduce your monthly payments, save on interest, or adjust your loan term, refinancing can be a powerful tool—but it’s not without its potential drawbacks.

| Pros | Cons |

|---|---|

| Lower interest rates | Potential for higher overall costs |

| Reduced monthly payments | Extended debt period |

| Opportunity to pay off loan sooner | Risk of becoming upside-down on the loan |

| Improved cash flow | Fees and charges associated with refinancing |

| Ability to remove or add a co-signer | Possible prepayment penalties |

| Consolidation of multiple car loans | Impact on credit score |

Let’s delve into each of these advantages and disadvantages to provide a comprehensive understanding of what refinancing your car loan entails.

Advantages of Refinancing Your Car Loan

Lower Interest Rates

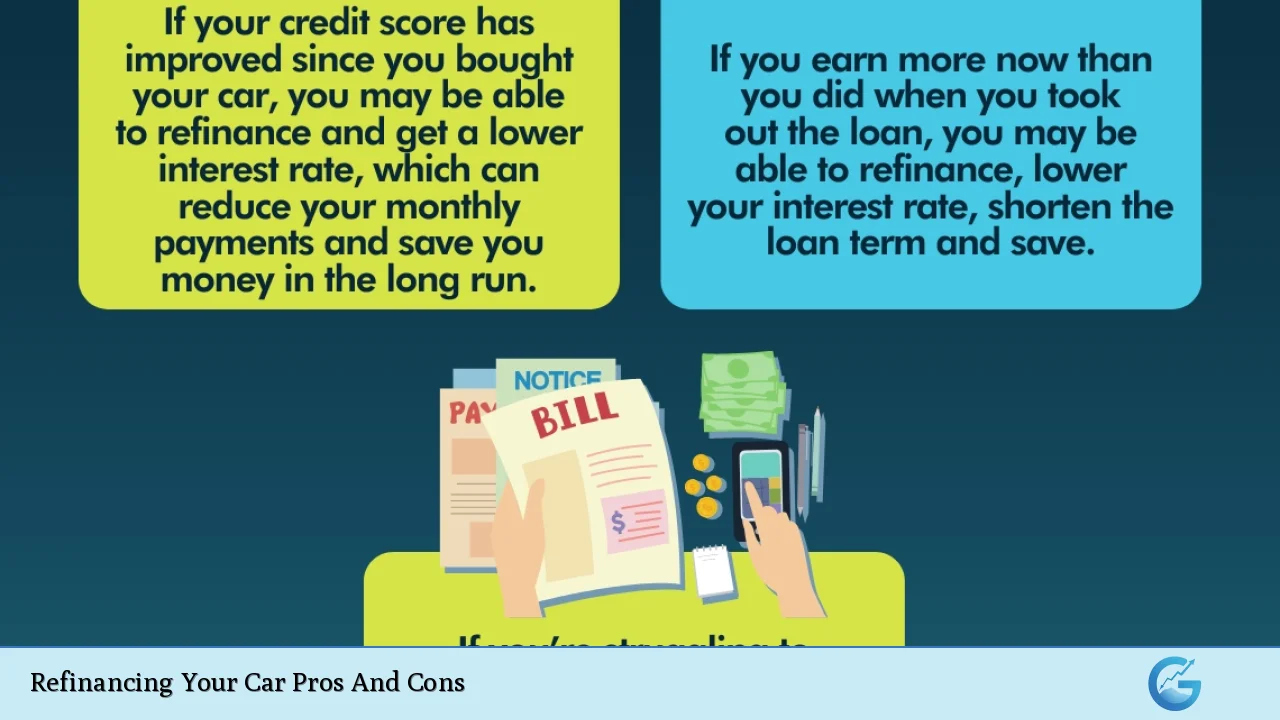

Securing a lower interest rate is often the primary motivation for refinancing a car loan. If market interest rates have dropped since you originally financed your vehicle, or if your credit score has improved, you may qualify for a significantly lower rate. This can lead to substantial savings over the life of your loan.

Benefits of lower interest rates include:

- Reduced total interest paid over the loan term

- More of each payment going towards the principal balance

- Potential for thousands of dollars in savings, depending on the loan amount and term

For example, if you initially financed $25,000 at 6% APR for 60 months and refinance to 4% APR after one year, you could save over $1,300 in interest over the remaining term of the loan.

Reduced Monthly Payments

Lowering your monthly car payment can provide immediate relief to your budget and improve your cash flow. This can be achieved through a combination of a lower interest rate and potentially extending the loan term. While extending the term may result in paying more interest over time, it can be a lifeline for those experiencing financial strain.

Advantages of reduced monthly payments:

- Increased financial flexibility

- Ability to allocate funds to other financial priorities

- Reduced risk of default on the loan

Consider a scenario where you’re paying $500 monthly on your current loan. Refinancing could potentially lower this to $400 or less, freeing up $100 or more each month for other expenses or savings.

Opportunity to Pay Off Loan Sooner

For those whose financial situation has improved since taking out the original loan, refinancing presents an opportunity to pay off the debt faster. By securing a lower interest rate and maintaining or even increasing your monthly payment, you can direct more money towards the principal balance.

Benefits of early loan payoff:

- Reduced total interest paid over the life of the loan

- Faster path to full vehicle ownership

- Improved debt-to-income ratio

Improved Cash Flow

Refinancing can significantly improve your monthly cash flow, providing financial breathing room. This is particularly beneficial for those who have experienced changes in their financial situation, such as a job loss or unexpected expenses. By reducing your monthly car payment, you can free up cash for other essential needs or financial goals.

Advantages of improved cash flow:

- Greater financial stability

- Ability to build an emergency fund

- Opportunity to invest in other areas, such as retirement savings or the stock market

Ability to Remove or Add a Co-signer

Refinancing offers the chance to restructure the loan agreement, which can include adding or removing a co-signer. This can be beneficial in various scenarios:

- Removing a co-signer who no longer wishes to be responsible for the loan

- Adding a co-signer to potentially qualify for better terms

- Releasing a co-signer from obligation if the primary borrower’s financial situation has improved

Consolidation of Multiple Car Loans

For those with multiple vehicle loans, refinancing can provide an opportunity to consolidate these debts into a single loan. This simplification can make managing your finances easier and potentially lead to cost savings.

Benefits of loan consolidation:

- Simplified payment process with one monthly payment instead of multiple

- Potential for a lower overall interest rate

- Easier tracking of your auto debt

Disadvantages of Refinancing Your Car Loan

Potential for Higher Overall Costs

While refinancing can lower your monthly payments, it may lead to paying more in total interest over the life of the loan if you extend the term. This is a crucial consideration that requires careful calculation to ensure the refinance truly benefits your financial situation.

Risks of higher overall costs:

- Extended loan terms resulting in more interest paid

- Short-term gains potentially leading to long-term financial strain

- Difficulty in accurately predicting long-term financial benefits

Extended Debt Period

Refinancing to a longer term can keep you in debt for a more extended period. This extended commitment to the loan can impact your ability to save or invest in other areas of your financial life.

Drawbacks of an extended debt period:

- Delayed financial freedom

- Increased vulnerability to changes in financial circumstances

- Potential overlap with the need for a new vehicle

Risk of Becoming Upside-Down on the Loan

Extending your loan term through refinancing can increase the risk of owing more on your car than it’s worth, a situation known as being “upside-down” or having “negative equity.” This can be particularly problematic if you need to sell or trade in the vehicle before the loan is paid off.

Consequences of negative equity:

- Difficulty selling or trading in the vehicle

- Potential for rolling negative equity into a new car loan, compounding the problem

- Increased financial risk in case of accident or total loss of the vehicle

Fees and Charges Associated with Refinancing

Refinancing isn’t free. Various fees can be associated with the process, which may offset some of the potential savings. These can include:

- Application fees

- Origination fees

- Title transfer fees

- State re-registration fees

It’s crucial to factor these costs into your calculations when determining if refinancing is financially beneficial.

Possible Prepayment Penalties

Some auto loans come with prepayment penalties, which are fees charged if you pay off the loan early. When refinancing, you’re essentially paying off the original loan, which could trigger these penalties.

Considerations regarding prepayment penalties:

- Need to review the terms of your current loan carefully

- Potential for penalties to negate refinancing benefits

- Importance of including these costs in refinancing calculations

Impact on Credit Score

The refinancing process typically involves a hard credit inquiry, which can temporarily lower your credit score. While the impact is usually minor and short-lived, it’s something to be aware of, especially if you’re planning other major financial moves in the near future.

Credit score considerations:

- Temporary dip in credit score

- Potential impact on ability to secure other loans or credit

- Importance of timing refinancing with other financial decisions

In conclusion, refinancing your car loan can be a powerful financial tool when used wisely. It offers the potential for significant savings and improved financial flexibility. However, it’s crucial to carefully weigh the pros and cons, considering your individual financial situation and long-term goals. By understanding the intricacies of auto loan refinancing, you can make an informed decision that aligns with your overall financial strategy.

Frequently Asked Questions About Refinancing Your Car Pros And Cons

- How soon after getting a car loan can I refinance?

While some lenders may allow refinancing immediately, it’s generally advisable to wait at least six months to a year. This allows time for your credit score to recover from the initial loan and for you to establish a payment history. - Will refinancing my car loan hurt my credit score?

Refinancing typically results in a hard credit inquiry, which can cause a small, temporary dip in your credit score. However, if refinancing leads to more timely payments, it can positively impact your credit in the long run. - Can I refinance if I have negative equity in my car?

It’s possible, but more challenging. Lenders are often hesitant to refinance loans with negative equity, and those that do may offer less favorable terms. You might need to bring cash to the table to cover the difference. - Is there a best time to refinance my auto loan?

The best time is when you can secure better terms than your current loan. This could be when interest rates drop, your credit score improves, or your financial situation changes significantly. - How much can I save by refinancing my car loan?

Savings vary widely depending on your current loan terms, new loan terms, and loan balance. Even a 1-2% reduction in interest rate can save hundreds or thousands of dollars over the life of the loan. - Are there any cars that can’t be refinanced?

Most lenders have restrictions on the age and mileage of vehicles they’ll refinance. Typically, cars older than 7-10 years or with over 100,000-150,000 miles may be difficult to refinance. - Can I refinance my car loan with bad credit?

It’s possible, but challenging. You may face higher interest rates or be required to have a co-signer. Improving your credit score before applying for refinancing is often beneficial. - What documents do I need to refinance my car loan?

Typically, you’ll need proof of income, proof of insurance, details about your current loan and vehicle (including VIN), and personal identification. Some lenders may require additional documentation based on their specific requirements.