A 529 savings plan is a tax-advantaged investment vehicle designed to help families save for future education expenses. These plans, sponsored by states or state agencies, offer a range of benefits but also come with certain limitations. Understanding both the advantages and disadvantages of 529 plans is crucial for making informed decisions about education savings strategies.

| Pros | Cons |

|---|---|

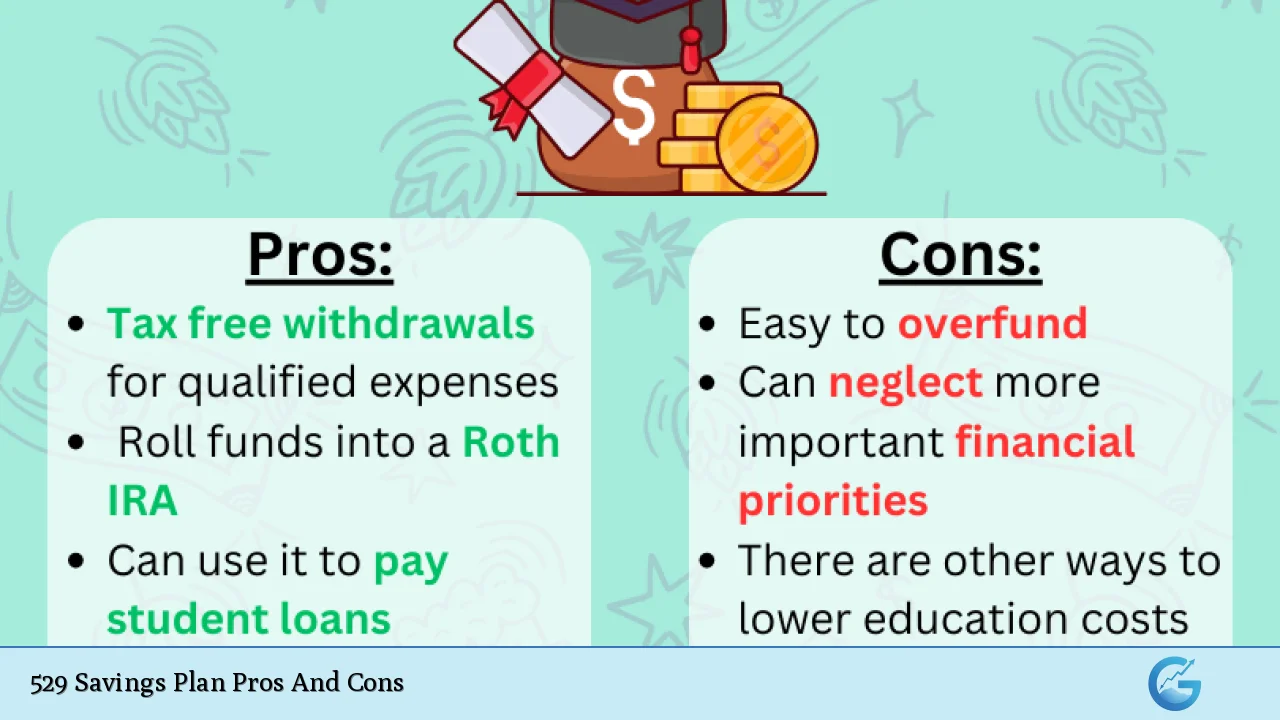

| Tax-free growth and withdrawals for qualified expenses | Limited investment options |

| High contribution limits | Potential for penalties on non-qualified withdrawals |

| State tax benefits in many states | Impact on financial aid eligibility |

| Flexibility in changing beneficiaries | Fees can vary and potentially be high |

| No income restrictions for contributors | Restrictions on investment changes |

| Estate planning benefits | State tax recapture risks |

| Control retained by account owner | Potential for over-saving |

Tax-Free Growth and Withdrawals

One of the most significant benefits of 529 plans is their tax-advantaged status.

While contributions are made with after-tax dollars, the earnings in the account grow tax-free at the federal level. Moreover, withdrawals used for qualified education expenses are also tax-free, providing substantial savings over time. This tax-free growth can significantly boost the overall return on investment, especially for those who start saving early.

High Contribution Limits

529 plans offer remarkably high contribution limits, often reaching hundreds of thousands of dollars per beneficiary. These limits are set by each state and typically align with the projected cost of attending the most expensive colleges in the country. For instance, many states allow total contributions of $300,000 to $500,000 per beneficiary. This high ceiling enables families to save aggressively for education without worrying about hitting contribution limits.

State Tax Benefits

In addition to federal tax advantages, many states offer additional tax incentives for contributions to their 529 plans. These benefits can come in the form of:

- State income tax deductions

- Tax credits

- Matching grants

As of 2024, over 30 states provide some form of tax benefit for 529 plan contributions.

Some states, like Indiana, even offer tax credits, which directly reduce your tax bill rather than just your taxable income. It’s important to note that while most states require you to contribute to your home state’s plan to receive these benefits, a few states offer tax benefits for contributions to any 529 plan.

Flexibility in Changing Beneficiaries

529 plans offer significant flexibility when it comes to changing beneficiaries. Account owners can change the beneficiary to another qualifying family member without incurring penalties or taxes. This feature is particularly useful in scenarios where:

- The original beneficiary receives a scholarship

- Decides not to pursue higher education

- Has leftover funds after completing their education

The ability to change beneficiaries allows families to efficiently manage education savings across multiple children or even generations.

No Income Restrictions for Contributors

Unlike some other education savings vehicles, 529 plans do not impose income restrictions on contributors. This means that high-income earners, who might be phased out of other education savings options, can fully utilize 529 plans. Furthermore, anyone can contribute to a 529 plan – parents, grandparents, other relatives, or even friends – making it a versatile tool for collective saving efforts.

Estate Planning Benefits

529 plans offer unique estate planning advantages. Contributions to a 529 plan are considered completed gifts for federal tax purposes, removing the assets from the contributor’s taxable estate. Moreover, 529 plans allow for a special five-year gift-tax averaging provision. This provision enables contributors to make a lump-sum contribution of up to five times the annual gift tax exclusion amount ($17,000 in 2024) without incurring gift taxes, effectively front-loading up to $85,000 per beneficiary ($170,000 for married couples).

Control Retained by Account Owner

Unlike custodial accounts, the account owner of a 529 plan retains full control over the assets.

This means that the account owner, not the beneficiary, decides when withdrawals are made and for what purpose. If the beneficiary decides not to pursue higher education, the account owner can change the beneficiary or use the funds for their own education. This level of control ensures that the savings are used as intended and provides peace of mind to contributors.

Disadvantages of 529 Savings Plans

Limited Investment Options

One of the primary drawbacks of 529 plans is the limited range of investment options available. Unlike a standard brokerage account where investors can choose from a wide array of stocks, bonds, and mutual funds, 529 plans typically offer a curated selection of investment portfolios. These often include:

- Age-based portfolios that automatically adjust asset allocation as the beneficiary approaches college age

- Static portfolios with fixed asset allocations

- Individual fund options

While these options are designed to cater to different risk tolerances and time horizons, they may not satisfy investors who prefer more control over their investment choices or those seeking to invest in specific sectors or companies.

Potential for Penalties on Non-Qualified Withdrawals

Using 529 plan funds for non-qualified expenses can result in significant penalties.

If withdrawals are not used for qualified education expenses, the earnings portion of the withdrawal is subject to federal income tax plus a 10% penalty. Qualified expenses include:

- Tuition and fees

- Room and board (with limitations)

- Books and supplies

- Computer equipment and internet access

- Up to $10,000 annually for K-12 tuition

- Student loan repayments (up to $10,000 lifetime limit)

The strict definition of qualified expenses and the potential for penalties can make 529 plans less flexible than other savings vehicles, especially if there’s uncertainty about future education plans.

Impact on Financial Aid Eligibility

529 plans can affect a student’s eligibility for need-based financial aid. The impact depends on who owns the account:

- Parent-owned 529 plans: Assessed at a maximum of 5.64% of the account value when calculating the Expected Family Contribution (EFC)

- Student-owned or UGMA/UTMA-owned 529 plans: Assessed at 20% of the account value

- Grandparent-owned 529 plans: Not reported on the FAFSA but distributions count as student income (assessed at up to 50%)

While the impact is generally less severe for parent-owned accounts, families should consider how 529 savings might affect overall financial aid strategies.

Fees Can Vary and Potentially Be High

The fee structure of 529 plans can vary significantly between states and even between investment options within the same plan. Fees to consider include:

- Enrollment fees

- Annual account maintenance fees

- Program management fees

- Underlying fund expenses

Some plans, particularly those sold through financial advisors, may have higher fees that can erode returns over time.

It’s crucial to compare fee structures across different plans and consider their long-term impact on investment growth.

Restrictions on Investment Changes

Federal regulations limit the frequency of investment changes within 529 plans. Account owners are typically allowed to change their investment options only twice per calendar year or upon a change in beneficiary. This restriction can be frustrating for investors who want to actively manage their portfolios or respond quickly to market conditions.

State Tax Recapture Risks

While state tax deductions or credits can be a significant benefit, they also come with a potential downside. Some states have “recapture” provisions that require residents to pay back previous tax deductions or credits if they:

- Roll over funds to another state’s 529 plan

- Take non-qualified withdrawals

- Move out of state

This recapture can negate the initial tax benefits and should be carefully considered, especially for those who may relocate or change plans in the future.

Potential for Over-Saving

While having excess funds in a 529 plan is generally preferable to having insufficient savings, it can present challenges. Over-saving in a 529 plan can lead to:

- Unused funds subject to taxes and penalties if withdrawn for non-qualified expenses

- Reduced flexibility in using the savings for other purposes

- Potential impact on financial aid for younger siblings if funds are not used by the original beneficiary

Families should carefully project education costs and consider diversifying their savings across different vehicles to maintain flexibility.

Frequently Asked Questions About 529 Savings Plan Pros And Cons

- Can 529 plan funds be used for international schools?

Yes, funds from 529 plans can be used at many foreign institutions that are eligible for federal student aid programs. However, not all international schools qualify, so it’s important to verify eligibility before using 529 funds abroad. - What happens if my child receives a full scholarship?

If your child receives a full scholarship, you can withdraw up to the scholarship amount from the 529 plan without incurring the 10% penalty on earnings. However, you will still owe income tax on the earnings portion of the withdrawal. - Can I have multiple 529 plans for the same beneficiary?

Yes, you can open multiple 529 plans for the same beneficiary, even in different states. This strategy can be used to maximize state tax benefits or access different investment options. - Are there age limits for 529 plan beneficiaries?

Generally, there are no age limits for 529 plan beneficiaries. You can open a 529 plan for a beneficiary of any age, including adults planning to return to school or even for yourself. - How do 529 plans compare to Roth IRAs for education savings?

While both offer tax-free growth, 529 plans are specifically designed for education expenses and offer higher contribution limits. Roth IRAs provide more flexibility for non-education expenses but have lower contribution limits and income restrictions. - Can 529 plan funds be used to repay student loans?

Yes, as of 2019, up to $10,000 from a 529 plan can be used to repay qualified student loans for the beneficiary and each of their siblings. This is a lifetime limit per individual. - What investment options are typically available in 529 plans?

Most 529 plans offer age-based portfolios, static allocation portfolios, and individual fund options. Some plans may also offer FDIC-insured savings accounts or stable value funds for more conservative investors. - How do market fluctuations affect 529 plan savings?

Like any investment, 529 plans are subject to market fluctuations. The impact depends on the chosen investment strategy and time horizon. Age-based portfolios typically become more conservative as the beneficiary approaches college age to mitigate market risk.

In conclusion, 529 savings plans offer significant advantages for education savings, particularly in terms of tax benefits and flexibility. However, they also come with limitations and potential drawbacks that must be carefully considered. Families should evaluate their specific financial situations, education goals, and risk tolerance when deciding whether a 529 plan is the right choice for their education savings strategy. By understanding both the pros and cons, investors can make informed decisions that align with their long-term financial and educational objectives.