A deferred compensation plan is a financial arrangement that allows employees to set aside a portion of their income to be paid out at a later date, typically during retirement. This strategy is often utilized by high-income earners and executives as a means to reduce current taxable income while saving for the future. While these plans can offer significant advantages, they also come with inherent risks and disadvantages that must be carefully considered. This article explores the pros and cons of deferred compensation plans, providing a comprehensive overview for individuals interested in finance, investment strategies, and wealth management.

| Pros | Cons |

|---|---|

| Tax deferral benefits | Risk of company bankruptcy |

| No contribution limits | Irrevocable decisions |

| Enhanced retirement savings potential | Lack of liquidity |

| Payout flexibility | Future tax implications |

| Attracts and retains talent | Potential for forfeiture |

| Improved cash flow management for employers | Complex regulations and compliance issues |

Tax Deferral Benefits

One of the most significant advantages of deferred compensation plans is the ability to defer taxes on the income set aside. Employees can reduce their taxable income in the year they contribute to the plan, allowing them to pay taxes only when they withdraw the funds, typically during retirement when they may be in a lower tax bracket.

- Immediate tax relief: By deferring compensation, employees can lower their current taxable income.

- Future tax savings: If an employee expects to retire in a lower tax bracket, they can save significantly on taxes by deferring income.

Risk of Company Bankruptcy

A major disadvantage associated with deferred compensation plans is that they are often unsecured. This means if the employer faces financial difficulties or declares bankruptcy, employees may lose their deferred compensation.

- Unsecured creditor status: Deferred amounts become part of the company’s assets and are subject to claims by creditors.

- Potential loss of savings: Employees risk losing their deferred income if the company cannot fulfill its obligations.

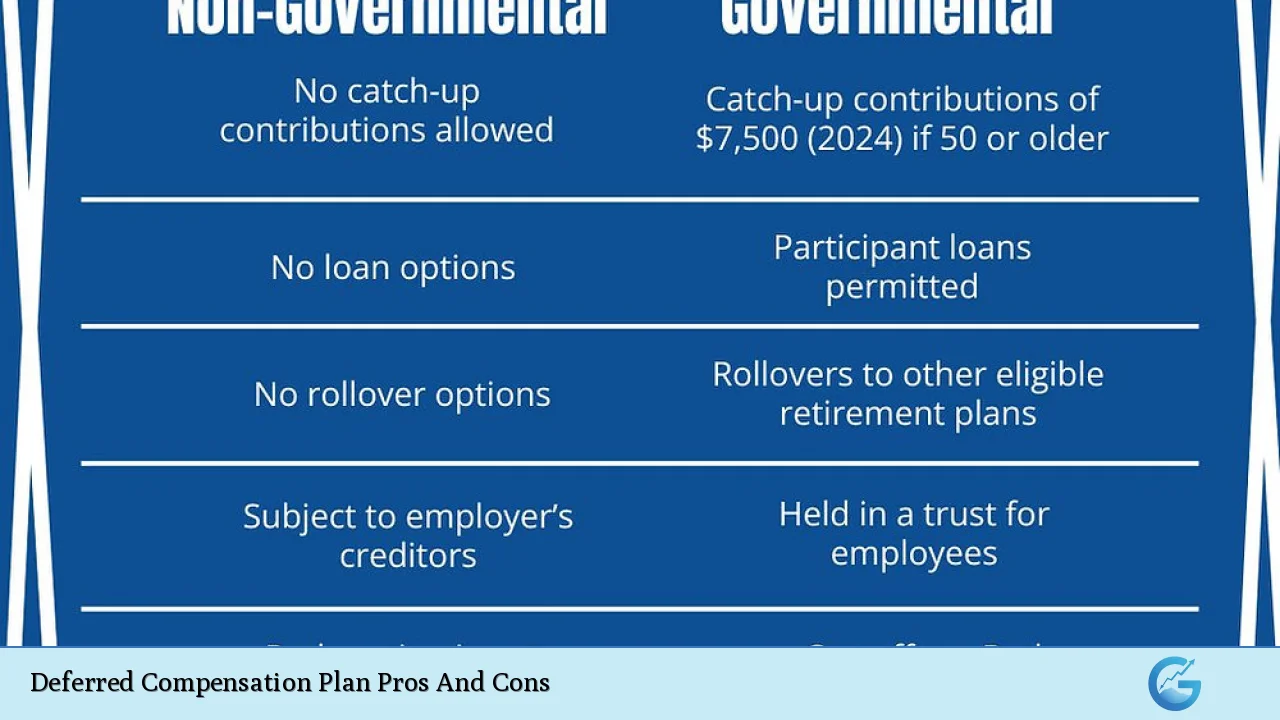

No Contribution Limits

Unlike traditional retirement accounts such as 401(k)s or IRAs, deferred compensation plans typically do not have contribution limits. This allows high earners to set aside substantial amounts for future use.

- Flexibility in savings: Employees can defer a large portion of their salary without restrictions.

- Maximized retirement funding: High-income individuals can significantly boost their retirement savings beyond standard limits.

Irrevocable Decisions

Once an employee opts into a deferred compensation plan and decides how much to defer, this decision is generally irrevocable for that year. This lack of flexibility can pose challenges if personal circumstances change.

- Limited adjustment options: Employees cannot easily change their deferral amounts or withdraw funds until specific conditions are met.

- Planning necessity: Careful planning is essential before committing to a deferred compensation plan.

Enhanced Retirement Savings Potential

Deferred compensation plans can substantially increase an employee’s retirement savings. Contributions grow tax-deferred until withdrawal, potentially leading to significant growth over time.

- Compounded growth: Funds invested in deferred compensation plans can accumulate interest or investment returns over time.

- Long-term financial security: These plans help ensure that employees have adequate resources during retirement.

Lack of Liquidity

Deferred compensation plans often lack liquidity, meaning employees cannot access their funds until they retire or meet specific conditions set by the plan.

- Access restrictions: Employees may not withdraw funds while still employed unless under hardship provisions.

- Financial planning challenges: This can complicate personal financial management and emergency funding needs.

Payout Flexibility

Many deferred compensation plans offer various payout options, allowing employees to choose how they receive their funds upon retirement.

- Tailored payment structures: Employees can opt for lump-sum payments or installment distributions based on their financial needs.

- Strategic tax planning: Flexible payout options allow retirees to manage their tax liabilities effectively.

Future Tax Implications

While deferring income can offer immediate tax benefits, it is crucial to consider future tax implications when funds are eventually withdrawn.

- Tax liability upon withdrawal: Withdrawals will be taxed as ordinary income in the year they are taken.

- Potential higher tax rates: If tax rates increase in the future, employees may face higher taxes on their withdrawals than anticipated.

Attracts and Retains Talent

Employers often use deferred compensation plans as a tool to attract and retain key talent within their organizations. These plans provide valuable incentives for high-performing employees.

- Competitive advantage: Offering such benefits can differentiate an employer in the job market.

- Employee loyalty: Deferred compensation encourages long-term commitment from key personnel.

Potential for Forfeiture

Depending on the terms of the plan, employees may risk forfeiting part or all of their deferred compensation if they leave the company before certain conditions are met.

- Golden handcuffs effect: Employees may feel compelled to stay with an employer solely due to deferred benefits.

- Loss of benefits upon departure: Leaving before vesting periods could result in significant financial loss.

Improved Cash Flow Management for Employers

For employers, offering deferred compensation plans can lead to better cash flow management by delaying payroll expenses associated with employee compensation.

- Budget-friendly option: Companies can manage short-term cash flow more effectively by deferring payments.

- Strategic financial planning: This allows businesses to allocate resources more efficiently while still providing competitive benefits.

Complex Regulations and Compliance Issues

Deferred compensation plans are subject to various regulations and compliance requirements that employers must navigate carefully. Failure to adhere to these rules can result in severe penalties.

- Regulatory scrutiny: Employers must ensure compliance with IRS regulations and other legal requirements.

- Administrative burden: Managing these plans requires careful oversight and expertise, which may strain smaller organizations.

In conclusion, while deferred compensation plans offer numerous advantages such as tax deferral benefits, increased retirement savings potential, and flexibility in payouts, they also present significant risks including potential loss due to company bankruptcy and lack of liquidity. Individuals considering participation in such plans should weigh these pros and cons carefully against their personal financial goals and circumstances. Proper planning and consultation with financial advisors are essential for making informed decisions about deferred compensation strategies.

Frequently Asked Questions About Deferred Compensation Plans

- What is a deferred compensation plan?

A deferred compensation plan allows employees to set aside part of their earnings for future payment, reducing current taxable income. - Who should consider a deferred compensation plan?

This plan is ideal for high-income earners looking to maximize retirement savings while minimizing current taxes. - What happens if my employer goes bankrupt?

If your employer declares bankruptcy, you may lose your deferred compensation as it is treated as unsecured debt. - Are there contribution limits?

No, unlike traditional retirement accounts, there are typically no contribution limits for deferred compensation plans. - Can I change my deferral amount once elected?

No, decisions regarding deferrals are generally irrevocable once made for that year. - What are the tax implications upon withdrawal?

Withdrawals from a deferred compensation plan are taxed as ordinary income at the time of distribution. - How do these plans help employers?

Deferred compensation plans help employers manage cash flow by delaying payroll expenses while attracting top talent. - Is there any risk involved?

Yes, there are risks including potential forfeiture of funds if leaving employment early and exposure to company financial instability.